May 16, 2025

Tariffs, rates, and the hidden costs of homeownership.

AAA expects travel to hit record highs this Memorial Day weekend. Our recommendation for anyone boarding a plane: stay clear of the "airport theory” TikTok challenge.

This week: inflation numbers cool, jobless claims stay steady, and the true cost of owning a home.

Fuel up! 🚀

Biz buzz

Jerome Powell can sleep easier this week

After much talk about the incoming impact of tariffs on inflation, last week brought two key reports on the effect so far.Both the Consumer Price Index and the Producer Price Index came in below market expectations. This is welcome news, as it gives the Federal Reserve a bit more breathing room and the ability to cut interest rates should they see weakness in the labor market.

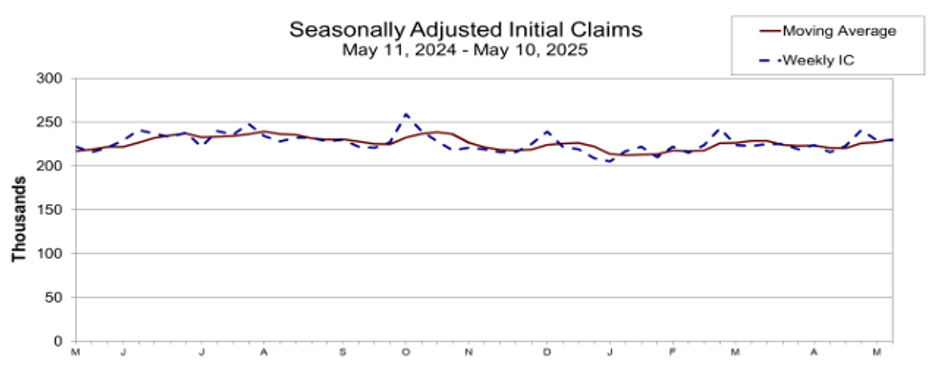

Labor market resiliency

The initial jobless claims report for the week ending May 10 showed that 229,000 people filed for unemployment benefits, unchanged from the previous week and in line with expectations. This stability in the labor market has been notable, offering a sense of predictability that has helped steady markets amid broader economic uncertainty.

Caffeinated trends

The true cost of homeownership

For many Americans, buying a home is a milestone symbolizing stability, investment, and personal success. However, for a growing number of homeowners, that milestone may come with a hidden cost: becoming “house poor.”

“House poor” refers to homeowners who spend such a significant portion of their income on housing related expenses (mortgage payments, property taxes, insurance, maintenance, etc.), that they struggle to afford other essentials, including food, health care, and savings.

While the issue is often associated with first-time home buyers or limited housing supply, there is growing concern about the financial strain faced by long-time, low-income homeowners.

According to Harvard’s Joint Center for Housing Studies, the number of cost-burdened homeowners between 2019 and 2022 (those who spend more than 30% of their income on housing) rose by 3 million to almost 20 million households.

Concerningly, the greatest increase was seen among households earning under $30,000 a year, who now face a cost-burden rate of over 70%. These aren’t just new buyers stretching to afford a mortgage; many are older homeowners on fixed incomes, people who bought their homes long ago but are now squeezed by rising costs that are out of their control.

Even people with low, locked-in mortgage rates aren’t spared from becoming “house poor.” Budgets are being strained by increasing property taxes and home insurance premiums, especially in areas vulnerable to extreme weather events.

For example, average insurance premiums rose 21% in 2023. With annual property taxes now averaging over $4,000, even homeowners who have paid off their mortgages are feeling the financial strain. Nearly 60% of homeowners over age 65 with incomes below $30,000 are considered cost-burdened. That figure rises to 95% if they still have a mortgage.

Adding to the challenge is the aging housing stock. The median U.S. home is now 64 years old, and maintenance costs are rising. The Federal Reserve Bank of Philadelphia has estimated that owner-occupied homes nationwide require about $98 billion in repairs. While home equity has grown substantially in recent years, tapping into it given the current market can mean higher rates or more expensive loans, both of which can be risky and inaccessible for lower-income owners.

Pandemic-era programs like the Homeowner Assistance Fund helped hundreds of thousands of households avoid foreclosure, but many of these supports have ended. While some assistance remains, such as the Low Income Home Energy Assistance Program (LIHEAP), these programs often reach only a small portion of those who need help.

On a more hopeful note, the Inflation Reduction Act unlocked billions in funding for energy-efficient home upgrades. These improvements can lower long-term utility costs for low-income households.

Homeownership has long been an aspirational path for people of all incomes to achieve personal and economic security for themselves and their families. Stabilizing low-income homeowners is essential to make that dream a lasting reality.

While The State of the Nation’s Housing 2024 report serves as a clear reminder that the pressures on this group are real and growing, so is the opportunity to make a difference. With the right mix of immediate support and long-term investment, we can help ensure that these households not only stay housed, but also hopeful. Ultimately, to Help Everyone Home means making it sustainable, not just attainable.

Pro on the road

Purchase season is here. Stay prepared by engaging with industry leaders and discovering what’s next. We’ll be at these top events—let’s connect!

May 20 – 21: Inman on Tour Miami – Miami, FL

June 2 – 5: NJ MBA Regional Conference – Atlantic City, NJ

June 8 – 10: Tennessee Bankers Association Annual Meeting – Marco Island, FL

Join us for meaningful conversations, valuable insights, and new opportunities to drive your business forward. We look forward to seeing you there.

Pro puzzles

Good luck!

This week's pro puzzle

2 Rockets