January 12, 2026

Why first-time buyers need more than lower rates.

New year, fewer goals? Researchers are finding that clinging to the wrong goals can actually drain our energy, whereas quitting – when done intentionally – can be surprisingly healthy. Perhaps this year, the most productive resolution will be knowing when to let go.

This week, we explore slipping worker confidence, AI’s impact on 2025 markets, and developments in home affordability.

Fuel up! 🚀

Bizz Buzz

Proposed institutional home buyer ban

The current administration recently announced plans to bar large institutional investors from purchasing additional single-family homes, citing concerns that corporate ownership has increased home prices and made homeownership less accessible for individual buyers.

The proposal would target private equity firms and real estate investment trusts that have acquired significant portfolios of rental homes over the past decade, which some analysts argue has reduced housing supply for individual buyers.

Implementation details are currently unclear, but the administration indicated it may seek Congressional support to codify such measures into law.

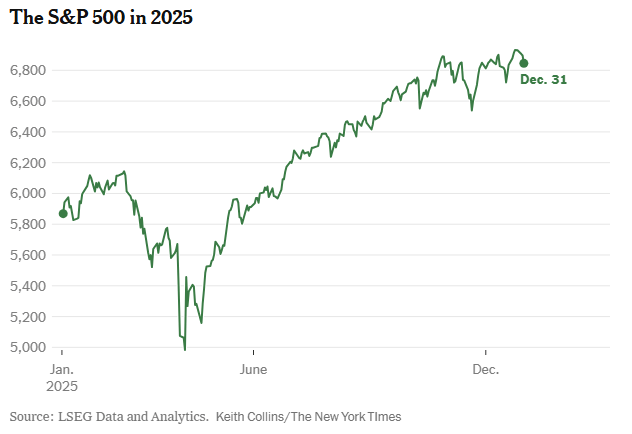

AI-fueled market gains mask growing risks

Though the path was volatile and uneven, U.S. stocks finished 2025 broadly in line with expectations. The S&P 500 rose 16.4%, largely driven by enthusiasm around artificial intelligence, with massive investments in data centers, software, and semiconductors fueling gains in a small group of technology leaders.

The so-called “Magnificent Seven” stocks, particularly Nvidia, accounted for a disproportionate share of the index’s performance, masking weaker returns across much of the wider market. This concentration has raised concerns about valuations and investor overreliance on continued AI optimism. Looking ahead, analysts cite economic cooling and policy uncertainty as risks that could cause the AI-led rally to lose momentum.

Caffeinated Trends

Down payment rates continue to rise

While mortgage rates and home supply have been trending in a positive direction for home buyers, saving for a down payment remains a major obstacle for those looking to achieve the dream of homeownership.

The U.S. Census reported homeownership levels had fallen to 65% in the second half of 2025, the lowest seen since pre-COVID. With the reduction in mortgage rates over the past year, buyers should be able to take advantage of additional savings. For example, putting 20% down on a $410,000 home brings the monthly payment down nearly $200 year-over-year. While home supply increased over the last few months of 2025 (12% higher year-over-year), prices have yet to see a substantial reduction.

When it comes to saving for a down payment, a typical home buyer usually needs 7 years to reach their goal. While this is still almost double the time needed pre-pandemic, there has been a reduction from 12 years down to 7 since 2022. Much of this stems from the personal savings levels seen by households over the past decade. Prior to 2020, households achieved a personal savings rate of 6.5% on average, with that number creeping even higher further back in the decade. Looking at 2025, the U.S. averaged a personal savings rate of about 5.1%, substantially down from levels seen in the past.

On top of U.S. households saving at a lower rate than before, the average down payment has actually risen quite a bit over the past few years. From the third quarter of 2019 to the third quarter of 2025, the average down payment more than doubled, jumping from $13,900 to $30,400. This has forced households to save at an even higher rate than before to achieve homeownership. Depending on the market, buyers may be forced to save nearly an entire year of income before venturing into the market.

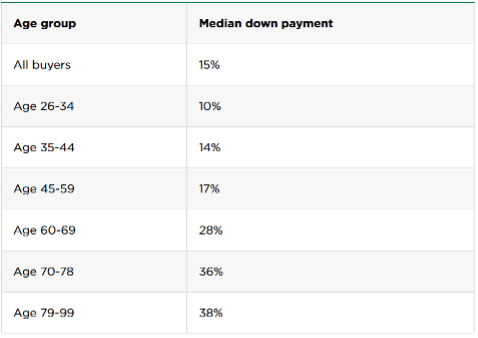

Younger or first-time home buyers seem the most affected by this increase in down payment amounts. Even when younger buyers are able to purchase a house, their median down payment comes in significantly lower than buyers in upper age groups. Even though there have been some positive developments in the market for home buyers, down payments continue to rise, making it even harder to enter the market for a home.

Just one solver was able to finish last week’s puzzle in under a minute – great work to our top solver, who came in at 42 seconds.

3 Rockets

This article is for informational purposes only, and is not a substitute for professional advice from a medical provider, licensed attorney, financial advisor, or tax professional. Consumers should independently verify any service mentioned will meet their needs.